Bonds Are Back? Perspectives From The Field

2022, in no uncertain terms, was a bad year for global bond markets. After years of high prices and low yields, the rapid rise of interest rates, intended to reduce inflation, impacted the bottom line of bond investors in a historical way.

Fortunately, the Fed’s approach seems to have made a sizable impact on inflation as the rolling 12 month CPI percentage change was 3.2% in July 2023 compared to 8.5% a year earlier. Importantly, we’re still above the Fed’s long-term target of 2% inflation, and the Fed has indicated that reducing to 2% will likely require additional intervention.

Consistent with our long-term strategic approach we remained invested, but not dormant. Many of our clients will benefit from the tax-loss harvesting done in 2022 for years to come, offsetting future capital gains and income.

Luckily, as you are reading this now, the worst is likely behind us and we’re hearing the sentiment “bonds are back!”

With the turmoil of 2022 left in the dust, peering through the front windshield, we see a much more favorable environment for bond investing with significantly higher income and the opportunity for capital appreciation if rates fall.

One Dimensional Fund Advisors article from Oct 2022 summarizes the relationship between rising rates and falling prices well, stating:

“Investors can think of this tradeoff as a pit stop in a Formula 1 race. The pit stop immediately causes the driver to fall back. However, fresh tires may help the driver win the race if there are enough laps left to catch the leader.”

_____________________________________________________________________________________________

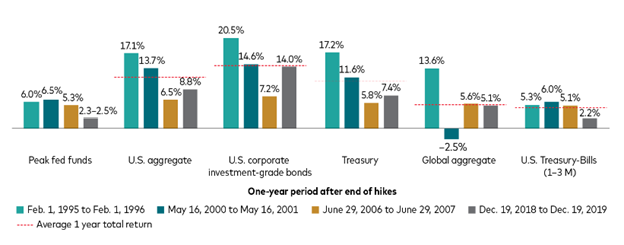

Bonds also tend to perform well after the Federal Reserve stops raising interest rates, as shown in the chart below:

The Fed’s language remains hawkish, indicating that more rate hikes are expected, but the moderating inflation numbers (as indicated by CPI) seem to indicate that these hikes will be limited. Vanguard analogized this to hitting cruising altitude on a plane:

“For most of the global bond market, that’s roughly where we are: near cruising altitude. We may hit some turbulence yet, but with respect to the U.S., we believe the Fed has moved on from playing catch-up with its policy actions to a period of fine-tuning, which likely translates into one or two more rate hikes this year before holding steady well into 2024.”

An article published by J.P. Morgan speaks to the fundamental truth that a decline in value creates a relatively more attractive investment opportunity. Considering a decline of 11.2% in 2022, as measured by the Bloomberg Global Aggregate Bond Index, the long-term upside of bonds has likely grown.

“As the dust settles, bonds are looking outright cheap relative to the past 20 years, with valuations in U.S. Treasuries and core fixed income a standard deviation below their long-run average. This has presented an attractive entry point for investors.”

_______________________________________________________________________________________________

Our view is that these positive sentiments should not be taken as a mass call to purchase more bonds in your portfolio. Rather, we believe it should offer some relief to anyone troubled by the experience of bond investing in 2022.

Woodward Financial Advisors maintains our belief that bonds are still the best diversifier to stock market risks, both through their consistent (and now higher) income and their imperfect correlation with stock market returns.

Relatedly, we also recommend utilizing higher yielding bank accounts and cash equivalents, too. Generally, these higher yielding options are money markets, short-term CDs, short-term treasuries, or a combination. If you’re curious how these accounts are insured, read our article from April 2023 on this topic.