Charitable Giving Strategies

Charitable Giving Strategies

Fall is easily my favorite season of the year. It brings pumpkin spice lattes, brightly colored leaves, and football nearly every day of the week! With Giving Tuesday right around the corner, fall is also an important time of the year for charitable giving, as many donors make their year-end gifts. From our perspective, it’s a great time to think about year-end tax planning, with charitable donations as a powerful tax planning tool.

Many people know about the potential to receive a tax deduction for gifts to charity, but it can get a little complicated from there. Navigating how much to give, whether to give cash or appreciated securities, and whether to give directly to an organization or to use a donor advised fund or other type of account can be overwhelming. Below, we’ve shared a high level summary of some of our favorite ways to maximize our clients’ charitable giving while minimizing taxes.

Cash Vs Appreciated Securities:

Long-time followers and clients of Woodward have likely heard our suggestions about donating appreciated securities, as this strategy is often more tax efficient than donating cash. When you donate appreciated securities to a qualified charity or to your Donor Advised Fund (DAF), the fair market value is deducted from your taxable income if you itemize (with some IRS limitations). In addition, neither you (in the future) nor the charity (now) will be taxed on the capital gain. Therefore, you can make a bigger impact with your donation by gifting your stocks rather than liquidating them and gifting the cash that remains after you have paid the capital gains tax.

In some cases, donating cash may still be the best route to fulfill your charitable inclinations. For example, if a stock is trading for less than what you paid for it, it’s usually better to sell the stock and donate the cash to charity. This allows you to take a tax loss on your tax return for that year and a potential deduction for your donation. Sometimes cash or a credit card for small gifts is also more convenient – the last time I saw someone ringing a bell outside the grocery store, they weren’t accepting shares of stock!

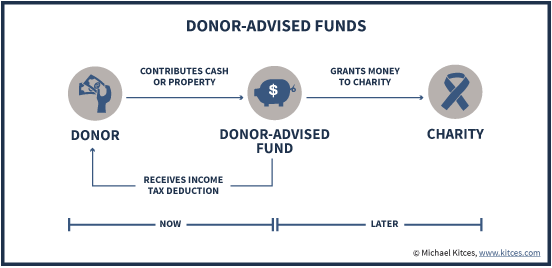

Donor Advised Funds:

Another tool that can help you achieve your charitable objectives while reducing your overall income tax burden is a donor advised fund (DAF). DAFs are accounts that can be funded with cash, appreciated stock, and other assets – and essentially function as your own personal giving account. Here a few benefits of using a DAF:

- The grantor (donor) receives a tax deduction for the value of the contribution (with some IRS limitations) in the year the contribution is made to the DAF. This enables you to take the tax deduction for your gifts all at once, even if you don’t plan to gift the funds immediately.

- For donors with few other itemized tax deductions, a DAF enables you to “bunch” your charitable deductions into one year, helping you to qualify to itemize your deductions, without the need to give more to your end charities in that year. It’s called “bunching” because you repeat this strategy every few years, itemizing in those years as you replenish your DAF for the interim years without a gift to your DAF.

- Funds contributed to a DAF can be invested for tax-free growth and allow you to spread your support of qualified charities over several years.

- DAFs are simple to establish and have low minimum contribution levels and low annual fees.

- For donors making many different charitable gifts, the tax reporting becomes much simpler with a DAF. The taxpayer needs to provide the sum contributed to the DAF and all subsequent grants to charities are not reported.

The use of DAFs can be an important component of your charitable gifting strategy and can be an effective tool when making year-end gifts.

Qualified Charitable Distributions:

Understanding the benefits of qualified charitable distributions starts with an understanding of required minimum distributions. Beginning at age 73, folks who hold tax-deferred retirement accounts, such as IRAs or 401(k)s, must begin taking a minimum annual distribution. Any distribution from these types of accounts increases total taxable income for that year.

A qualified charitable distribution (QCD) enables individuals 70 ½ years old or older to fulfill their charitable goals and, for those ages 73 and up, partially satisfy their required minimum distribution by a direct transfer of up to $100,000 to charity. One benefit of completing a QCD, is that it does not increase taxable income (meaning higher tax rates and other related taxes can be avoided). Additionally, the donation counts toward your required minimum distribution amount, reducing your total taxable distributions. A quick example might make qualified charitable distributions a little more clear. Let’s say you are 75 years old, and have a required distribution of $20,000. If you make a $5,000 gift directly to the Ronald MacDonald Foundation from your IRA, you are now only required to take $15,000 from your IRA this year, and will only be taxed on this $15,000 of additional income. The only catch is that you aren’t able to send those funds to a Donor Advised Fund (see prior section). A qualified charitable distribution needs to go directly to your end charity.

Concluding Thoughts:

While giving your hard-earned money to charities that mean something to your family isn’t something anyone does for tax purposes alone, a little planning around taxes can help make a bigger difference for the causes you care about, and help you save on taxes at the same time. If you would like to learn more about these strategies, we would love to hear from you!

Resources: